For a refresher on where we left O.P. and M.J. Van Sweringen, see Part 1 and Part 2 of “Train Dreams”

By Pete Beatty

“I feel that I am one of those who are not influenced by dollars. There is a profit beyond a certain point that is no inducement to me. I haven’t made up my mind whether to be poor is to be rich or to be rich is to be poor, but I’m inclined to believe the latter.” —O.P. Van Sweringen, 1925

As the Van Sweringen brothers worked to realize their dream of a union terminal on Public Square in downtown Cleveland, they did not neglect the other arms of their business empire. Their suburban developments on the east side of Cleveland were thriving. Shaker Heights saw its population increase tenfold from 1920 to 1930, and an even larger development to the east was underway.

The new Shaker Country Estates, even more expansive than Shaker Heights, would be marketed to an even more affluent clientele. More and more Americans were getting rich in a booming decade. The Dow Jones Industrial Average nearly quadrupled in the second half of the ‘20s. A decent-sized share of that newfound wealth was a necessity for those seeking an address in Shaker Country Estates, where land began at $2,250 an acre.

At the heart of the new development was a staggering 600-foot wide set of boulevards, designed to accommodate a four-track rapid transit line, two highways, and a set of one-way local roads. Cleveland’s well-to-do might still commute to the center city via train, but the automobile was quickly gaining ground.

Cleveland was always a distant second to Detroit as an automobile hub. But in the first three decades of the twentieth century, more than $20 million worth of automobiles were manufactured in the city. In addition, steel and parts for cars and truck poured out of Cleveland’s mills and factories. In 1922, Detroit’s Fisher Body Company opened a plant on the city’s east side that would soon employ 7,000. In 1926, Fisher became a part of General Motors, cranking out hundreds of auto bodies each day for GM vehicles.

O.P. (left) and M.J. take a drive with a business partner in 1917.

Outside of Cleveland, O.P. and M.J. remained focused on railroads. They had purchased the 500-plus miles of the Nickel Plate Road in 1916, and put the line in the hands of John J. Bernet, a New York Central vice president who had come to the brothers via their railroading fairy godfather, Alfred H. Smith of the Central. Bernet had started out as a telegraph boy in tiny Farnham, New York, and rapidly climbed the ranks. He shared modest origins, serious ambition, and a talent for building successful businesses with the brothers.

The Vans installed Bernet as president of the Nickel Plate, and he quickly moved to improve and expand the road. He hired a crew of like-minded executives, who rapidly set to building sidings, fixing track, and installing powerful modern engines and switches. These tweaks, complemented by a newly vigorous management style, were the beginning of what was to be known as “the Van Sweringen way”—a tradition of no-nonsense, cost-effective operation.

As Bernet remade the Nickel Plate into a consistently profitable business, the brothers laid plans for something far more ambitious than the terminal they envisioned for Public Square. The nationalization of American railroads from 1917 to 1920 had shaken up an industry that was never especially organized. Congress passed the Esch-Cummins Act in 1920, charging the Interstate Commerce Commission with making sense of the tangle of trackage—and ownership—that spanned the nation.

[blocktext align=”left”]The Van Sweringens were planning to join the heavyweight class.[/blocktext]The epic legislative and lobbying drama that grew out of the Esch-Cummins Act has filled many books of history. The ICC was empowered to cap the earnings percentage of railroads and possibly redistribute excess profits among weaker roads. Bankers and other backers of railroads piggy-backed on the Red Scare that gripped the US in the wake of the Russian Revolution, a spate of bombings and alleged terrorist plots. Groups like the National Association of the Owners of Railroad Securities lobbied hard against plans to “russianize the railroads.”

The transportation reform that was passed was far from laissez-faire; the ICC found itself deciding the shape of individual roads and larger systems. Of particular interest to the Van Sweringens was the industrial heart of America, east from the Mississippi to major Atlantic ports, north from the coal mines of Appalachia to the foundries and forests of Michigan. Before the war and nationalization, three major systems dominated this region: the Baltimore & Ohio, the New York Central, and the Pennsylvania. The Van Sweringens were planning to join the heavyweight class.

+++

Two deals closed for the Van Sweringens in July 1922. They took control of the Lake Erie & Western (707 miles of track) and the Toledo, St. Louis & Western, better known as the Clover Leaf Road (453 miles). Both were purchased under arrangements similar to the Nickel Plate—an initial cash outlay and an agreement to make subsequent payments over a lengthy stretch of time. Once again, the Van Sweringens did not have the cash on hand. But the brothers, by now millionaires several times over, found securing huge lines of credit easy.

The better part of a decade had passed between O.P and M.J.’s first railroad acquisition, and they had no thought of waiting to buy again. In 1923, the brothers struck an impossibly complex deal with the Huntington family, the largest individual stockholders of the Chesapeake & Ohio Railroad. Treading carefully, and creatively, the Vans dodged ICC regulation by having one of their subsidiaries purchase 96 percent of the Huntington family stock for $80 a share, while a separate Van Sweringen concern bought the remaining 4 percent for $566.67 per shae. Of course, neither of the Van Sweringen companies actually had the cash to back those purchases.

Conveniently, the newly enlarged Nickel Plate—incorporating the LE&W and Clover Leaf—had just raised $8.66 million through a fresh bond issue. On paper, the bond was intended to improve the trackage of the Nickel Plate. But instead the stock issue funded the purchase of the C&O, a road that hauled coal out of Appalachia. That coal could be loaded onto Nickel Plate trains bound for industrial centers like Cleveland, Chicago, St. Louis, Toledo, Detroit, and Buffalo. Chesapeake trains also ran to the Atlantic ports of Hampton Roads, Virginia.

Before any kind of consolidation of their rail holdings was contemplated, the Van Sweringens were buying again. Later in 1923, the Vans acquired the Pere Marquette, a line that crisscrossed Michigan and southern Ontario. The brothers also grabbed the Chicago & Eastern Illinois, providing a direct link between Chicago and St. Louis. In 1924, the Van Sweringen organization gobbled up the Erie, a system with subsidiaries of its own, which connected Buffalo to New York City and Newark.

All of these deals were highly leveraged—just enough voting stock was acquired to effectively control railroads, with a minimal outlay of cash. This Van Sweringen trademark made buying new properties easy, but it also meant the brothers were building an empire they could hardly afford. As long as the markets stayed bullish, and the railroads posted big profits, the Van Sweringen Express would chug right along.

[blocktext align=”right”]All of these deals were highly leveraged—just enough stock was acquired for control, with a minimal outlay of cash.[/blocktext]While national rail route mileage had already peaked, the Vans and their 10,000 miles were posting steady return. Trains hauled a large majority of all of America’s cargo, especially in an era before pipelines were constructed to move oil and other liquid fuels. Beyond the pure business of building suburbs and hauling freight, the Vans controlled a vast forest of stocks in a feverish bull market. They had gone from small-time real estate operators in 1915 to the masters of a billion-dollar empire in 1925.

By 1935, the brothers would be bankrupt.

+++

The Vans took a breather from acquiring railroads in the second half of the 1920s. There was plenty to keep them busy. The Terminal Tower development was rising in downtown Cleveland, and the massive expanse of the Shaker Country Estates would soon fill in with the Jazz Age equivalent of McMansions. The brothers prepared an application to the Interstate Commerce Commission to consolidate their welter of trunk lines and branches—the enhanced Nickel Plate, the Chesapeake & Ohio, the Pere Marquette, the Erie, and all their collected subsidiaries—into a major new system to rival the Pennsylvania, New York Central, and Baltimore & Ohio.

The application for consolidation was made to the ICC in 1925; it would take nearly three years for the overmatched agency to sort through the maze of holding companies and render a verdict on whether the consolidation of so many railroads under Van Sweringen control complied with anti-trust regulations. When the decision finally came down in the spring of 1928, it was not the answer O.P. and M.J. were hoping for. Their fourth eastern system was never to be.

The ICC ruling was not a crushing blow, but it did mean that the brothers had an immediate problem. The brothers had been hoping to realize close to $60 million in new stock issues from the flurry of railroad consolidations and new holding companies in their proposed mergers. The ICC’s judgment left them about $30 million lighter than expected in stocks, and also managing close to $53 million in short-term debts. Buying on credit has a way of adding up quickly.

The solution, as always, was a new holding company. The Alleghany Corporation—named for the highest point along the C&O’s tracks through the Appalachians—was chartered in January 1929. Alleghany served two functions: it would conveniently shield several of the Vans’ new purchases from ICC regulation, and it would be their biggest stock issue yet.

Alleghany would also employ a classic Van Sweringen trick: the Vans and their inside circle would maintain control of an $85 million capitalization with a minimum of cash. More than two-thirds of Alleghany’s funding came from non-voting shares. The remaining amount of stock did come with votes, but the majority of that voting stock was sold to the Van Sweringens in exchange for “selling” their railroads—which they owned, if just barely—to the Alleghany Corporation, which they also owned.

The stock went public and predictably soared. The common stock, with a par value of $20, climbed as high as $56. The brothers could pay their bills with plenty of liquidity left over. And surely profits would soon be rolling in from their railroads and the new Shaker developments—almost an afterthought compared to trains covering half a continent.

+++

Even before Alleghany had gone public, O.P. was preparing the next in a succession of wildly ambitious moves. The next target for the Van Sweringens would be the Missouri Pacific, itself a conglomerate totaling more than 12,000 miles of rail from St. Louis to Salt Lake City, crisscrossing the Plains and sweeping south through Texas, reaching all the way to the border. The MoPac was a major system unto itself, and adding it to the existing Van Sweringen lines would make the brothers the owners of the largest rail company in the nation.

[blocktext align=”left”]The brothers were on the verge of establishing the first coast-to-coast railroad system in American history.[/blocktext]Through the Alleghany Corporation and its countless subsidiaries, the Vans gobbled up stock in the MoPac. As rumors of their takeover bid spread, prices rose. The brothers and their partners doubled down, issuing more than $100 million in Alleghany stocks and bonds as the calendar turned to 1930. The stock market crash of October had rattled some, but O.P. and M.J. were not overly concerned. They would do their part to bolster the economy by carrying on business as usual. By March of 1930, they effectively controlled the Missouri Pacific, although at a steep price. The ICC would have to be appeased, and the excessive leverage meant a minor shock could cause outsized problems. But the brothers were on the verge of establishing the first coast-to-coast railroad system in American history.

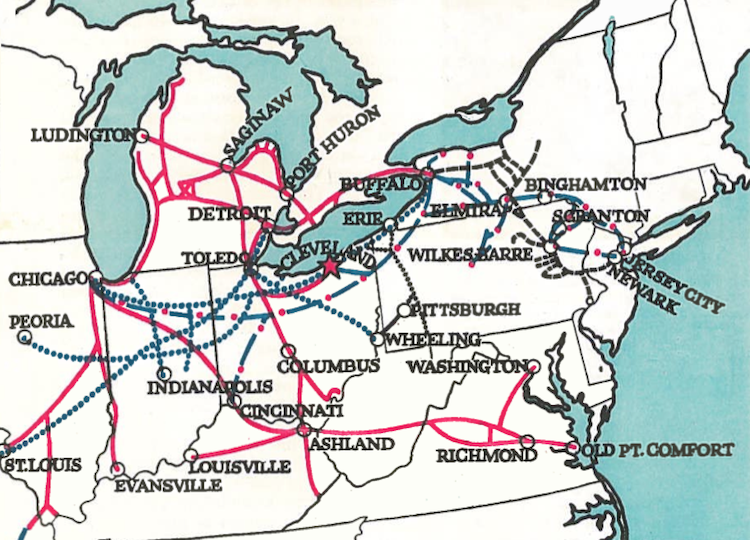

A map from Fortune magazine in 1934, showing the heart of the Vans’ railroading empire.

With the addition of the Missouri Pacific and its scores of subsidiaries, the Van Sweringen empire contained at least 275 companies, connected by dotted lines, stock swaps, and byzantine charters that were impossible to comprehend, and constantly shifting.

The Vaness Company was the capstone of the pyramid. The brothers held 80 percent of the shares. The remainder was held by a small circle of Van Sweringen insiders. The Vaness Company owned 71.3 percent of a paper company that held 100 percent of Cleveland Terminals Building Company, which voted 100 percent of Cleveland Hotel Company and the Higbee Company. The Cleveland Terminals Building Company also spoke for 35.7 percent of the Alleghany Corporation, which held a 46.3 stake in the Missouri Pacific.

Vaness also fully controlled the Van Sweringen Company, which in turn controlled the Shaker Company; other subsidiaries of Vaness included Metropolitan Utilities, which was an umbrella holding company that folded in Cleveland Traction Terminals Company, Cleveland Interurban Railroad Company, Traction Stores Company, the Cleveland Railway Company, and the Cleveland Youngstown Railroad. All this does not even touch upon the Vans’ interests in coal and trucking.

These paragraphs were tiring enough to write; imagine the nightmare of actually running such an unruly assortment, most of which were complex enough on their own. But as the Depression deepened and markets trembled, the undoing of the Van Sweringens would come from where they first started: Cleveland real estate.

Well in advance of the Union Terminal’s formal opening in 1930, the Van Sweringens and their business intimates moved into lavishly appointed offices on the 36th floor, lined with oak from England’s Sherwood Forest, and done up in typically stodgy Van Sweringen style. Their move into the Terminal Tower was accompanied by another reorganization. In the wake of the successful Alleghany stock issue, the brothers and their inner circle decided to create another monster holding company.

This newest creation would be called simply the Van Sweringen Corporation; this was the paper company that would control 100 percent of the Cleveland Terminal Buildings Company, the heart of the brothers’ hometown real estate properties. The new corporation’s stock issue was to raise $30 million for the Van Sweringens, earmarked for the further development of their real estate holdings in Cleveland. That $30 million was actually only half of what O.P. had hoped for. In the wake of the fall stock crash, and with murmurs that the Cleveland real estate market was beginning to freeze up, usually reliable J.P. Morgan shied away from underwriting Van Sweringen Corporation issue.

The brothers and their vast holdings were still viewed as a relatively safe bet, even as the financial turbulence of the previous fall lingered. The Guaranty Trust Company stepped in for Morgan, and $30 million of bonds with a 6 percent rate of return were issued. But with the market increasingly wobbly, the bank pushed the Vans to offer an unusual concession: a half-million shares of Alleghany stock from the brother’s holdings would remain in escrow until half of the $30 million in bonds had been paid off. There was an odd codicil to this stipulation—if the value of 500,000 shares of Alleghany stock dropped below $15 million, O.P. and M.J. were on the hook for the difference.

+++

[blocktext align=”right”]A $6 million shortfall was the beginning of the end for O.P. and M.J.[/blocktext]In May 1930, Alleghany stock traded at $26. On October 22, it bottomed out at $10.25 a share. The half-million shares of stock intended to ballast the Van Sweringen Corporation bonds were worth far less than the required $15 million. Mantis and Oris were obliged to commit their own assets to make up the deficit. The difference amounted to less than $6 million, hardly spare change but comparatively modest for operators who routinely struck eight-figure deals.

But this $6 million was the beginning of the end. The Vans were ceaselessly inventive in attempting to fend off ruin, but it was all in vain—and not simply because of the cratering Alleghany stock. Once the depression arrived, their reliance on inflated stock prices and layer upon layer of paper holding companies was no longer viable.

In the aftermath of the Alleghany stock crash, the brothers borrowed $39.5 million from a group of New York banks—there was no chance of another public stock issue, which could have panicked shareholders in other Van Sweringen entities, and causing a further collapse in share prices. That $39.5 million loan required virtually all of the brothers’ business empire as collateral. And just like that, the banks owned the Van Sweringens. The insinuation that had long dogged the brothers—that they were the creations of New York money—was finally true.

The Vans might have survived the Depression, despite its profoundly bad timing. If their railroad empire had earned enough profits, or if the Shaker Country Estates had flourished, they might have paid off their debts. But the economic slowdown of 1929 had worsened into the worst depression in American history. Business ground to a halt, in nearly every walk of life. Railroad revenues turned from black to red, and few people dared to buy or build upmarket homes.

Subsidiaries all across the Van Sweringen realm began to implode, each wipeout jeopardizing the interlinked web of holding companies. By late 1931, the Depression could no longer be dismissed as a routine fluctuation, and the federal government made available huge amounts of money to troubled businesses through the Reconstruction Finance Corporation. Van Sweringen railroads drew close to $60 million in these emergency loans.

[blocktext align=”left”]Subsidiaries all across the Van Sweringen realm began to implode.[/blocktext]In the spring of 1932, two major Cleveland banks went under. The Guardian Trust Company and the Union Trust held close to $20 million in loans to the Van Sweringens—money that actually belonged to the bank’s customers. The brothers had not been paying interest on those loans. Their reputation as square dealers was soon under a withering assault. As their magic disappeared, so did the tolerance of the press and public for the Van Sweringen’s not-infrequent lapses in business ethics.

The brothers in a moment of good humor during the 1933 Pecora hearings.

In 1933, O.P. and M.J. were dragged before the Senate Committee on Banking and Currency—better known as the Pecora commission, for the crusading government counsel Ferdinand Pecora who helmed the inquiries. Pecora’s grilling did not lead to any specific charges, but it cast a bright light on some of the less noble tactics the brothers had called upon in their desperate fight to save their empire.

The Van Sweringens had bought so much so haphazardly, and borrowed so widely, that they found themselves stuck in a maze, unable to exit without leaving creditors or themselves bankrupt. In the words of journalist John T. Flynn, in a scathing 1934 New Republic piece entitled “The Betrayal of Cleveland,” it was “inevitable that men who conduct business in this manner will find themselves after a while lost in a maze of conflicting responsibilities and that the ordinary guide posts of morality will become obscured.”

[blocktext align=”right”]“I’d rather have just paid the bill …”[/blocktext]The lowest moment was perhaps O.P.’s indictment by a Cuyahoga County grand jury for his role in a ill-advised attempt to cover up over the dire straits of the Union Trust, run by his close associate Joseph Nutt. O.P. had permitted an undocumented, short-term loan of $10 million in paper holdings to Union, so that the bank could pass a 1931 audit. This was unethical, and only made Union’s eventual failure more of a surprise to deposit holders. O.P. would be acquitted, but the incident loudly repudiated the “Van Sweringen Way.”

+++

“I’d rather have just paid the bill …”—O.P. Van Sweringen

The brothers managed to delay total collapse until May 1935, using every bit of cash and equity they could summon to fend off their creditors . Their massive debt to New York banks was in default. Their assets—a mammoth railroad empire ailing from debts and deficits all its own, their sprawling real estate holdings in Cleveland, and their stocks—were bound for the auction block.

Here O.P. managed one of his greatest, and most futile, feats. He allied himself with George Tomlinson, a shipping baron, and George Ball, an Indiana tycoon in the field of canning jars (Ball State University bears his name). Convincing the two men that the auction represented a chance for a rare bargain, O.P. authored his final corporate confection: the Midamerica Corporation. Of course, because the brothers were broke, they held no equity in Midamerica, but Ball and Tomlinson were willing to bankroll a last-ditch attempt to regain control of the Van Sweringen holdings.

[blocktext align=”left”]Friends calculated that O.P. would need to net $15 million per year for the rest of his life merely to pay off his debts.[/blocktext]Improbably, the hail mary succeeded. The banks were eager to wash their hands of the default-riddled railroads and lifeless real estate properties. The entire Van Sweringen kingdom was sold at a New York bank auction to Midamerica for $3.1 million. But the massive outstanding debts to creditors still loomed; any success the brothers found through Midamerica would only go toward chipping away at a mountain of debt.

O.P. would have to face that monumental task alone. On December 12, 1935, M.J. died after a two-month illness. His heart, always weak, had slowly faltered.

Oris mourned his brother deeply for a time, but eventually launched himself at the massive challenges facing his beleaguered empire. Van Sweringen business associates calculated that O.P. would need to earn more than $15 million per year, after taxes, to have any hope of retiring his various debts to banks in his lifetime. Despite a modestly improved economic climate, the Van Sweringen domain was still crumbling inside and out. Most of the Cleveland real estate holdings declared bankruptcy in the year following M.J.’s death; the very last of the last-ditch attempts to prop up some of the more troubled railroads were not successful. A new Senate investigation of the Van Sweringens was under way.

O.P. would not live to the inquiry’s conclusion. Less than a year after his brother’s death, Oris P. Van Sweringen died of a heart attack aboard a train in Hoboken, N.J. just after noon on Monday, November 23. His final day had been spent en route to New York for meetings with the bankers who owned his huge debts.

+++

94 passenger trains left Cleveland every day in 1922. By 1930, it was 85. In the heart of the Depression that number sank to 78. Even during the boom years of World War II, the traffic dropped to 63 trains a day. By the early 1970s, eight passenger trains left the city every day. By the end of that decade, the number was two. It has held steady ever since.

The Terminal Tower was riddled with vacancies, from empty storefronts on its concourses to platforms bereft of train service, as soon as it was born. The sprawling Shaker Country Estates was girded with roads and utility lines, but no residents or taxpayers. Even before O.P.’s death, a massive property tax assessment for the development was overdue. The Van Sweringen railroad system had posted a $86 million profit in 1929. In 1932, it lost $4.4 million. Their mansion at Daisy Hill was auctioned off after O.P.’s demise. As the suburbs rolled east, the 500-acre property was parceled off for development, and eventually the house itself was downsized, not worth the cost of upkeep. At a liquidation sale, the brothers’ furniture alone sold for $85,000, including their 80-legged dining table and 147 antique chairs.

+++

The Van Sweringen brothers have been forgotten, largely because they died without a fortune to bequeath. But Cleveland still resides in the wake of their ambition. Our city was remade by their developments, both downtown and in Shaker Heights. We live in their unfinished dreams.

Like many of the financiers and businessmen ruined by the Great Depression, the Van Sweringens saw their carefully crafted name damaged beyond repair. In 1935, before either brother’s death, a newspaper columnist speaking at the City Club could joke that the Vans’ Terminal Tower was “the highest thing in Cleveland, except for the pile of defaulted bonds they built.”

[blocktext align=”right”]We live in the unfinished dreams of the Van Sweringen brothers.[/blocktext]But in their brief heyday at the end of the 1920s, as the Terminal Tower opened for tenants and before their over-leveraged house fell, the brothers could sit in their skyscraper suites and look out their realm. Their railroads were knitted across half the nation, and the possibility of spanning the continent from sea to sea was within reach. The brothers had risen improbably from very modest beginnings to unimaginable success. Just as unimaginable was their cruel, rapid fall.

The first act of the Van Sweringens’ drama was marked by profound good luck. The brothers came of age in a time and place where their vision of a white-collar utopia was received rapturously by well-to-do Clevelanders eager to settle away from the squalor of the city. O.P. and M.J. carried their ambition to a national level through their ingenious, and sometimes unscrupulous, dealings in railroads and industry.

And just as their good luck amplified their innate talents into a billion-dollar empire, they also received an outsized share of the colossal bad luck of the Great Depression. They strove mightily to right themselves, but their fragile, flawed business practices could not withstand the strain.

Appropriately, at the foot of the Terminal Tower—in what was once Higbee’s, a Van Sweringen holding and the prize tenant of their transit complex—a casino beckons, 24 hours a day.

Pete Beatty is the Editorial Director of Belt.

Works consulted:

Daniel J. Boorstin, The Americans: The Democratic Experience

Ian S. Haberman, The Van Sweringens of Cleveland: The Biography of an Empire

Herbert H. Harwood, Invisible Giants: The Empires of Cleveland’s Van Sweringen Brothers

Kenneth T. Jackson, Crabgrass Frontier: The Suburbanization of the United States

Louise Jenks, O.P. and M.J.

Kenneth L. Kolson, Big Plans: The Allure and Folly of Urban Design

Julia C. Ott, When Wall Street Met Main Street: The Quest for an Investors’ Democracy

William Ganson Rose, Cleveland: The Making of a City

Ronald R. Weiner, Lake Effects: A History of Urban Policy Making in Cleveland, 1825-1929

Richard White, Railroaded: The Transcontinentals and the Making of Modern America

“The Story of the Rapid Transit,” Van Sweringen Company publication

“The Heritage of the Shakers” Van Sweringen Company publication

“History of the Nickel Plate Road,” Nickel Plate Road Historical and Technical Society

Periodicals: Journal of Architectural Education, Journal of Land & Public Utility Economics, Nation’s Business, Fortune, Ohio State Engineer, Harper’s, The New Republic, New York Times, Cleveland Press, Cleveland News, Cleveland Plain Dealer, American Magazine.

Special thanks to Ware Petznick at the Shaker Historical Society and Tim Beatty at the Western Reserve Historical Society for their help.